How Much Will an Investor Pay for My House?

Selling a home is one of the biggest financial decisions you will ever make. While the traditional route involves real estate agents, open houses, and months of waiting, selling to a real estate investor offers a different path. It promises speed, convenience, and cash. But one question looms larger than any other: How much will an investor pay for my house?

If you are expecting full retail market value, you might be disappointed. However, if you understand how investors calculate their offers, you can see the value in the trade-off. This guide dives deep into the numbers, the formulas, and the logic behind investor offers so you can decide if this route is right for you.

Understanding the Real Estate Investor Mindset

To understand the offer, you first need to understand the buyer. Unlike a family looking for a forever home, an investor is running a business. They aren’t buying your house because they love the kitchen backsplash; they are buying it to make a profit.

Investors typically fall into two main categories:

- Flippers: They buy distressed properties, renovate them, and sell them for a profit quickly.

- Buy-and-Hold Investors: They buy properties to rent out for long-term cash flow.

Both types of investors need to buy at a discount to make the numbers work. They take on significant risk—market fluctuations, unexpected repair costs, and holding costs—so their offer price must insulate them from these dangers.

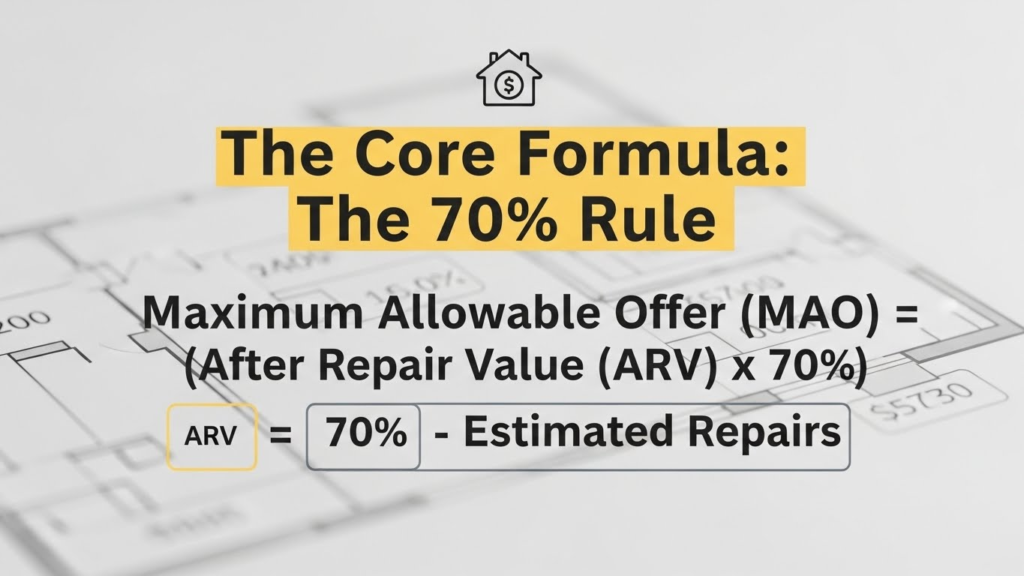

The Core Formula: The 70% Rule

When asking “how much will an investor pay for my house,” the most common answer revolves around the 70% Rule. This is the industry standard for house flippers.

The formula looks like this:

Maximum Allowable Offer (MAO) = (After Repair Value (ARV) x 70%) – Estimated Repairs

Let’s break down these NLP (Natural Language Processing) terms so you understand exactly what they mean.

After Repair Value (ARV)

This is not what your house is worth today. It is what your house would be worth if it were completely renovated to match the best comparable homes (comps) in your neighborhood. Investors look at recently sold homes that have new roofs, modern kitchens, and updated flooring to determine this number.

Estimated Repairs

This is the cost to get your house from its current condition to that ARV standard. Investors are thorough here. They calculate costs for materials, labor, permits, and unexpected overages.

The 70% Factor

Why 70%? Why not 80% or 90%? That missing 30% isn’t pure profit. It covers:

- Closing Costs: Buying and selling fees.

- Holding Costs: Taxes, insurance, and utilities paid while renovating.

- Cost of Money: Interest on hard money loans used to buy the property.

- Profit: The actual money the investor takes home for their work.

A Real-Life Example of the 70% Rule

Let’s say the nicest renovated house on your street just sold for $300,000. That is your ARV.

Your house needs a new roof, a kitchen update, and new flooring. The investor estimates repairs at $40,000.

Using the formula:

($300,000 x 0.70) – $40,000 = Offer Price

$210,000 – $40,000 = $170,000

In this scenario, an investor would likely offer you around $170,000 for a house that could eventually be worth $300,000.

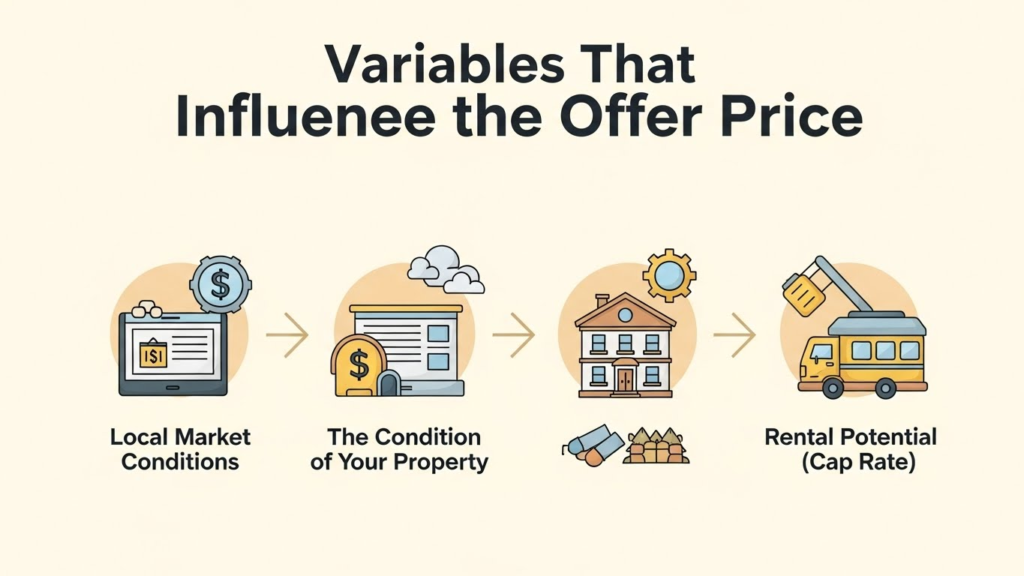

Variables That Influence the Offer Price

While the 70% rule is a standard benchmark, it is not a law of physics. The answer to “how much will an investor pay for my house” can fluctuate based on several variables.

1. Local Market Conditions

In a hot seller’s market where inventory is low, investors may be willing to accept thinner profit margins. They might bump that 70% up to 75% or even 80% to secure a deal. Conversely, in a slow market or a recession, they might drop to 65% to protect themselves.

2. The Condition of Your Property

This is the biggest lever.

- Heavy Rehab: If your home has structural issues, foundation problems, or fire damage, the risk is higher. Investors will budget for “worst-case scenarios,” driving the offer down.

- Cosmetic Updates Only: If the house just needs paint and carpet, the repair costs are predictable. Investors can often pay more because the risk of hidden costs is lower.

3. Rental Potential (Cap Rate)

Buy-and-hold investors (landlords) look at different metrics than flippers. They care about cash flow. They might pay more if the property is “turnkey” (ready to rent immediately) or if it is located in a high-demand rental area. They analyze the Capitalization Rate (Cap Rate), which measures the return on investment based on rental income.

4. Who You Are Selling To

- iBuyers (Instant Buyers): Companies like Opendoor or Offerpad use algorithms. They often pay closer to market value but charge high service fees (5%–14%) and demand credits for repairs after inspection.

- Local Wholesalers: These are middlemen who get your house under contract and sell the contract to another investor. Their offers are often the lowest because they need to leave room for the end buyer’s profit plus their own fee.

- Direct Cash Buyers: These are the actual flippers or landlords. Cutting out the wholesaler can sometimes net you a slightly higher offer.

The “Cost of Selling” Comparison

When you see the investor’s offer of $170,000 versus the Zillow estimate of $300,000, it’s easy to feel insulted. But comparing these two numbers directly is a mistake. You are comparing apples to oranges because you are ignoring the costs of a traditional sale.

To truly answer “how much will an investor pay for my house,” you must look at the Net Proceeds.

Traditional Sale Costs (The Retail Route)

If you sell on the open market for $300,000 (assuming you did the repairs yourself first), here is what comes out of your pocket:

- Repairs: You have to spend the $40,000 cash upfront to get that price.

- Realtor Commissions: Typically 6% of the sale price ($18,000).

- Closing Costs: Usually 1%–3% for sellers ($6,000).

- Holding Costs: Mortgage, tax, and utility payments while the house sits on the market for 3-6 months ($5,000+).

Total Deductions: $69,000.

Net Proceeds: $300,000 – $69,000 = $231,000.

Investor Sale Costs (The Cash Route)

- Repairs: $0 (Sold “as-is”).

- Realtor Commissions: $0.

- Closing Costs: Investors often pay these for you ($0).

- Holding Costs: $0 (Closes in 7–14 days).

Net Proceeds: $170,000.

The Gap

In this example, the difference is about $61,000. You are paying $61,000 for the convenience of selling instantly, avoiding the hassle of contractors, and not having strangers walk through your bedroom during open houses. For many sellers facing foreclosure, divorce, or an inherited property they can’t manage, that speed and certainty is worth the price difference.

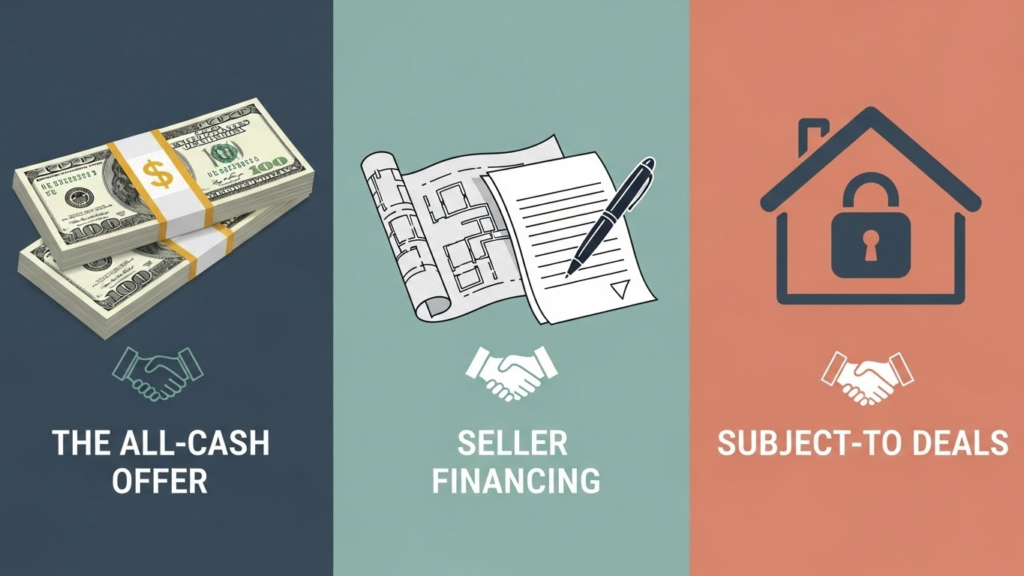

Different Types of Investor Offers

It is important to note that not all cash offers are structured the same way. When you ask, “how much will an investor pay for my house,” the answer might depend on the specific strategy they propose.

1. The All Cash Offer

This is the standard deal. You get a check at closing. It is the lowest offer amount but carries the least risk and highest speed.

2. Seller Financing

Sometimes an investor will offer you a higher price if you agree to “be the bank.” Instead of giving you all the cash upfront, they pay you a down payment and then monthly payments with interest. If you don’t need all the cash immediately, this can actually net you more than the market value over time due to interest.

3. Subject To Deals

In this scenario, the investor buys your house “subject to” the existing mortgage. They take over your payments but do not officially assume the loan. This is common for sellers with little to no equity who need to move quickly. The “price” paid here is essentially debt relief.

How to Get the Best Price from an Investor

Just because investors have formulas doesn’t mean you can’t negotiate. If you want to maximize how much an investor will pay for your house, follow these actionable tips.

1. Know Your Numbers

Do your own homework. Look up recent sales of renovated homes in your area (ARV) and get a general contractor to give you a rough quote on repairs. If an investor claims repairs will cost $80,000 but you have a quote for $50,000, you have leverage to negotiate a higher price.

2. Shop Around

Never accept the first offer. Reach out to multiple investors. Competition breeds better pricing. If Investor A offers $150,000 and Investor B offers $160,000, you can go back to Investor A and ask them to beat it.

3. Clean Up the Clutter

While you don’t need to renovate, a clean house presents better than a dirty one. If an investor can clearly see the floor and walls, they are less likely to overestimate repair costs to cover “unknowns.”

4. Highlight the Positives

Don’t just let them find the flaws. Point out the new HVAC system, the recent roof patch, or the quiet neighborhood. Remind them of the value they are getting.

5. Be Honest About Flaws

This sounds counterintuitive, but trust builds deals. If you hide a leak, the investor will find it during their inspection and likely slash their offer drastically or walk away. Being upfront allows them to calculate accurate numbers from day one.

Red Flags to Watch For

When searching for “how much will an investor pay for my house,” be wary of offers that seem too good to be true. Scammers and predatory wholesalers exist.

- The “Bait and Switch”: An investor gives you a high verbal offer over the phone. Once you sign a contract, they inspect the house and demand a $20,000 price reduction days before closing.

- Kitchen Table Closings: Always use a reputable title company or real estate attorney to close the deal. Never sign the deed over to someone at your kitchen table without a formal escrow process.

- Vague Contracts: Ensure the contract has a clear closing date and specifies who pays the closing costs.

When Should You Sell to an Investor?

Selling to an investor isn’t for everyone. If you have a pristine home, plenty of time, and want every last dollar of equity, list it with a real estate agent.

However, you should seriously consider an investor offer if:

- The House Needs Major Work: You don’t have the cash or energy to manage a renovation.

- You Need Cash Fast: You are facing foreclosure, tax liens, or need to liquidate assets for a medical emergency.

- You Inherited an Unwanted Property: You live out of state and don’t want to manage a vacant house.

- You Are Going Through a Divorce: You want a clean, quick break to split assets and move on.

- You Have Problem Tenants: The house is occupied by non-paying tenants, and you are tired of being a landlord.

The Psychological Value of a Cash Offer

While we have focused heavily on the math, the answer to “how much will an investor pay for my house” also involves psychological currency.

What is the price of your stress? What is the value of your time?

When you list a home traditionally, you are signing up for uncertainty. A buyer might make an offer, but then their financing falls through three weeks later. An inspection might reveal mold, forcing you back to the negotiating table. You might pay the mortgage on an empty house for six months.

An investor offer buys you certainty. It converts an illiquid, problematic asset into cash in as little as seven days. For many sellers, that peace of mind is worth the discount.

Calculating Your Personal “Walk-Away” Number

Before you call an investor, determine your bottom line.

- Calculate your mortgage payoff amount.

- Add any liens or taxes owed.

- Add the minimum amount of cash you need to move to your next living situation (deposit, first month’s rent, moving truck).

This total is your “Walk-Away Number.” If an investor’s offer meets or exceeds this number, it is a viable solution for your problem. If the offer falls short, you may need to consider other options, such as a short sale or listing with an agent who specializes in distressed properties.

Deep Dive: How Different Markets Impact Investor Pricing

Real estate is hyper-local. The answer to “how much will an investor pay for my house” changes depending on your zip code.

The Urban Core

In dense city centers where land is scarce, investors are often aggressive. They might pay 80% of ARV because they know the demand for housing is insatiable. Even a small profit margin in a high-value area results in a large paycheck.

Suburban Neighborhoods

These are the bread and butter for family home flippers. The 70% rule is strictly adhered to here. Investors rely on “comps” from similar subdivisions. If your house is the only one not renovated in a nice subdivision, it is a prime target for investors.

Rural Properties

Investors are cautious in rural areas. Homes sit on the market longer (lower liquidity). An investor might demand a deeper discount—perhaps 50% or 60% of ARV—to compensate for the risk that it might take a year to resell the property.

Case Study: The Inherited Hoarder House

To illustrate how this works, consider the case of the “Smith Family.” They inherited their aunt’s home, which was filled with decades of clutter and had not been updated since 1970.

- Market Value (Renovated): $250,000

- Repair/Clean-out Costs: $60,000 (It needed dumpsters, professional cleaning, plus full rehab).

- Traditional Agent Advice: “Clean it out, paint it, and we can list it for $160,000 as a fixer-upper.”

- Investor Offer: $115,000 Cash, purchase “as-is” with all clutter remaining.

The family did the math. To list it for $160,000, they would pay 6% commission ($9,600) and closing costs ($3,000), netting $147,400. But they would have to spend weeks hauling junk and paying for dumpsters.

They chose the investor offer of $115,000. They walked away with a check and never had to lift a single box. The investor took the risk, did the hard work, and earned their profit. The family bought their freedom from the burden.

Final Thoughts: Is It Worth It?

Ultimately, the question “how much will an investor pay for my house” is about balancing priorities.

If your priority is MAXIMUM DOLLARS, hire an agent, renovate the house yourself, and wait for the perfect buyer.

If your priority is MINIMUM STRESS AND MAXIMUM SPEED, an investor is your best solution.

Investors provide a valuable service in the real estate ecosystem. They provide liquidity to owners who are stuck. They revitalize neighborhoods by fixing up eyesores. And they offer a streamlined exit strategy that the traditional market cannot match.

By understanding the 70% rule and the costs associated with selling, you can enter negotiations with confidence. You won’t be insulted by a low offer; you will understand the math behind it. You will be able to spot a fair deal when you see one, and you will be empowered to make the choice that is best for your financial future.

If you have a house that has become a burden, don’t let it weigh you down. Crunch the numbers, reach out to local investors, and see what your property is worth in cash today. It might just be the fresh start you have been looking for.